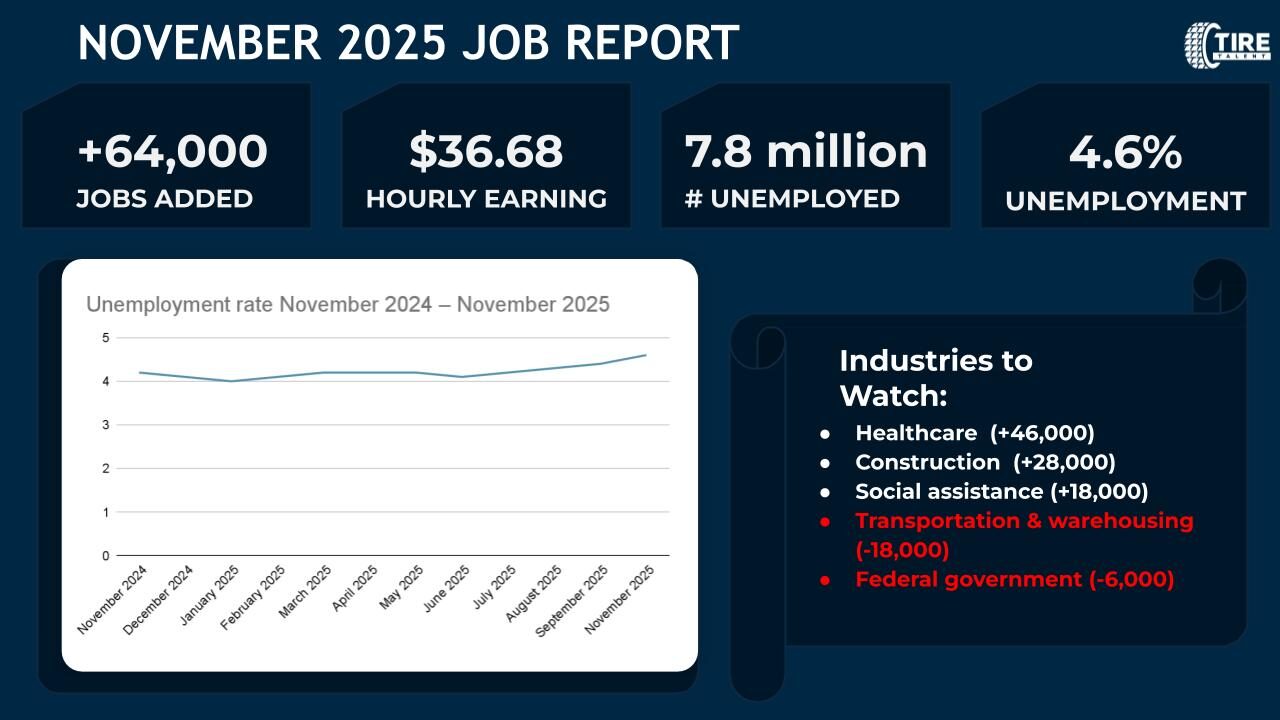

U.S. job growth slowed further in November 2025, with employers adding 64,000 jobs, extending a stretch of weak hiring that has shown little net progress since April. The unemployment rate rose to 4.6%, up from 4.2% a year earlier, leaving 7.8 million people unemployed, according to the Bureau of Labor Statistics.

While hiring continued in healthcare and construction, job losses in transportation, warehousing, and the federal government highlight a labor market that is cooling unevenly rather than collapsing, consistent with broader media and market assessments.

Key Highlights

November’s data reinforces a trend of slow hiring, rising joblessness, and growing underemployment, even as layoffs remain contained.

- Unemployment increased to 4.6%, up from 4.2% last November.

- 7.8 million unemployed, up from 7.1 million a year ago.

- Long-term unemployment held at 1.9 million, accounting for 24.3% of all unemployed.

- Short-term unemployment (<5 weeks) rose by 316,000 to 2.5 million, signaling fresh job losses.

- Labor force participation steady at 62.5%.

- Employment-population ratio unchanged at 59.6%.

Underemployment Is Rising

A notable development in November was the sharp rise in workers employed part time for economic reasons.

- Part-time for economic reasons: 5.5 million, up 909,000 from September.

- Indicates reduced hours, slower demand, and employer caution rather than mass layoffs.

This trend is consistent with a “low firing, low hiring” labor market.

Sector Movement: Narrow Gains, Broader Weakness

Hiring remained concentrated in a few sectors, while several labor-intensive industries continued to contract.

Job Gains

- Healthcare: +46,000

- Construction: +28,000 (led by nonresidential specialty trades)

- Social assistance: +18,000

Job Losses

- Transportation & warehousing: –18,000

- Down 78,000 since February peak

- Federal government: –6,000

- Down 271,000 since January due to deferred resignations

Most other sectors including manufacturing, retail, wholesale trade, professional services, and leisure & hospitality showed little to no change.

Wages and Hours

- Average hourly earnings: +$0.05 to $36.86

- 3.5% year-over-year growth (slowing trend)

- Production & nonsupervisory pay: +$0.11 to $31.76

- Average workweek: up slightly to 34.3 hours

- Manufacturing hours: flat at 40.0, overtime unchanged

Wage growth continues, but at a moderating pace.

Looking Ahead: Stability on the Surface, Strain Underneath

November’s report confirms a labor market that is not recessionary, but increasingly strained. Hiring is weak, unemployment is rising year-over-year, underemployment is accelerating, and job gains are narrowly concentrated.

With transportation and warehousing shrinking, federal employment falling sharply, and private-sector hiring uneven, employers are adapting by cutting hours instead of cutting headcount.

As we head into 2026, the labor market appears to be shifting from expansion to management mode prioritizing cost control, flexibility, and retention over growth.