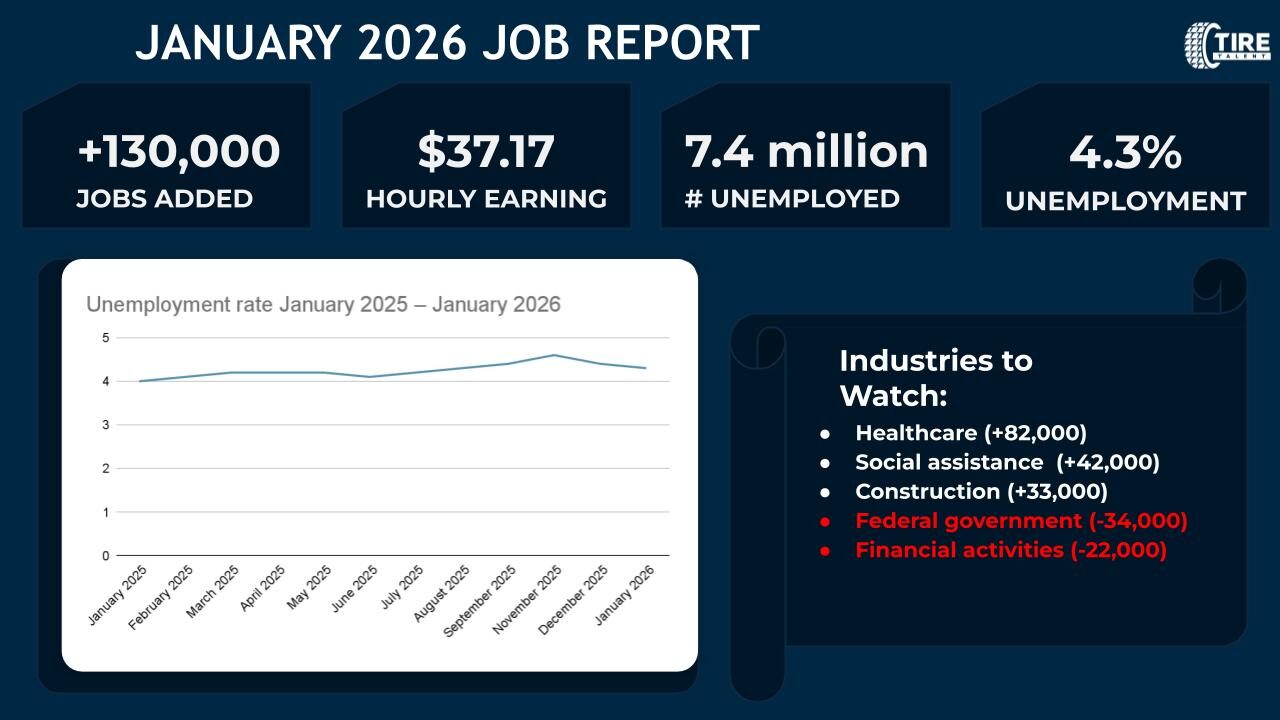

The U.S. labor market closed out 2025 on a steady but significantly slower note. According to the latest Employment Situation report from the Bureau of Labor Statistics (BLS), the era of rapid post-pandemic expansion has transitioned into a period of “economic normalization.”

For those in the tire sector from the factory floor to the retail counter this report signals a year ahead defined by inventory discipline, value-driven consumerism, and a focus on operational efficiency.

2025 vs. 2024: The Big Picture

Total nonfarm payroll employment rose by just 50,000 jobs in December, while the unemployment rate held steady at 4.4%. To understand the scale of this slowdown, look at the annual comparison:

|

Metric |

2024 Performance |

2025 Performance |

|

Total Job Gains |

2.0 Million |

584,000 |

|

Avg. Monthly Growth |

168,000 |

49,000 |

|

Market Tone |

Aggressive Expansion |

Cautious Stability |

This deceleration reflects the cumulative impact of higher interest rates and a broader cooling of the industrial sector. For the tire industry, this environment suggests softer new vehicle sales and a heightened need for cost control.

Retail Sector: A Shift in Consumer Spending

The retail trade saw a decline of 25,000 jobs in December. While electronics and appliance retailers saw modest gains, the losses were heavy in warehouse clubs, supercenters, and general merchandise stores.

The Industry Impact:

For tire dealers, this indicates a “value-first” consumer. As discretionary income tightens, customers are more likely to:

- Defer non-essential maintenance.

- Shop for promotional deals.

- Trade down from premium brands to Tier 3 or Tier 4 budget tires.

Manufacturing: Stability Over Growth

Manufacturing employment remained largely unchanged in December. While the industry isn’t seeing mass layoffs, hiring has effectively frozen.

- Average Workweek: Edged down to 39.9 hours.

- Overtime: Remained flat at 2.9 hours.

The Takeaway for Manufacturers: The focus has shifted from expanding capacity to maximizing productivity. Expect 2026 to be a year of careful production planning and strict inventory discipline to avoid oversupply in a cooling market.

Wage Growth and “Hidden Slack”

Average hourly earnings rose 0.3% in December (reaching $37.02), bringing the year-over-year increase to 3.8%. While this is still above pre-pandemic averages, the pace is moderating.

However, beneath the 4.4% headline unemployment rate, “hidden slack” is emerging:

- Long-term unemployment is up by 400,000 year-over-year.

- Part-time for economic reasons has surged by 980,000.

- Labor force dropouts who still want a job increased by 684,000.

This suggests that while the market isn’t “crashing,” the pool of available labor is growing, which may further ease the upward pressure on wages in 2026.

Strategic Outlook: The 2026 Roadmap

As we move into a “low-growth, high-efficiency” environment, here is how industry players should pivot:

- For Manufacturers: Prioritize lean manufacturing. Align production schedules with “steady-but-slow” replacement demand rather than forecasting for aggressive growth.

- For Distributors: Reassess your product mix. With underemployment rising, demand for budget-friendly tires will likely outpace premium lines. Ensure your warehouse is stocked to meet the “value” demand.

- For Retailers & Dealers: The “war for talent” has cooled, but specialized technicians are still a rare commodity. Instead of high-cost external hiring, use the current wage stability to invest in upskilling and retaining your current team.

Marketing Strategy: Safety and value are your best-selling points. Emphasize financing options like “Buy Now, Pay Later” to help cautious consumers manage essential tire replacements.